Global Corporate Bonds – Attractive Yields but Thin Risk Premium

Caution warranted

|

|---|

| Bull Points | Bear Points |

|---|---|

| 1. US economy still remains solid | 1. Global growth ex-US is below trend |

| 2. Inflation is receding, but more to prove | 2. Credit valuations perhaps appear rich |

| 3. Rate cuts expected | 3. Significant geopolitical worries |

| 4. Corporate fundamentals still remain decent and technicals supportive | 4. Earnings growth is a concern, especially in Europe |

2023 proved to be a rather volatile year across rate and credit spread markets. We noted a number of factors conspired to whipsaw both government bond yields and corporate bond spreads over the period. Continued developed market central bank rate hikes into the summer, the regional banking crisis that gripped the US during 1Q 2023, and the end of the Federal Reserve’s (Fed) rate hiking cycle in July 2023 served to take risk assets and investors on a wild ride that ultimately resulted in very strong returns for government and corporate bonds. The volatility in rates has continued into the early part of 2024 but corporate spreads have remained range-bound, and tight, as the US economy continues forward. The strength of the US economy is somewhat surprising in the face of 550 bps of hikes over the past two years, and even more so considering that growth in Europe, the UK, China, and Japan still remains on a decline. US GDP and jobs growth in the first two months of the year has been quite solid, and while the Fed has made significant progress in the inflation fight, we see that there is more work to be done as evidenced by the higher than expected print in January. Was this a fluke due to seasonal adjustments? Or will this persist and cause the Fed to stay higher for longer? Only time will tell but our inclination is that further significant declines in inflation absent a recession will be hard fought. The market tends to agree, as expected rate cuts priced into the market by year end have fallen to about 3.5 from 6 or more just a couple of months ago.

Given this expectation, we remain concerned that the lagged effects of monetary policy tightening are still likely to weigh on economic activity, hence our down in risk credit positioning. The US economy continues to be sustained by the dwindling amount of excess savings remaining as well as consumers living beyond their means. Expectations in the market are high however; we expect the Fed will cut to lower real rates to keep the momentum going now that inflation has been reduced. However, the cost of capital for businesses, especially small to mid-size businesses, has already risen markedly. We believe refinancing of short-term maturities over the past few years should provide some breathing space, but maturity walls are likely to come into focus as we progress through the year. The Russell 2000 index is down 15% from its late 2021 high and earnings are declining, while we find that the tech-heavy S&P 500 index continues to make new highs and obscure the lack of breadth across the market. Further, earnings growth in the European market remains quite negative despite stock markets performing well. The expectation of significant rate cuts by central banks and the AI frenzy in the tech space have spurred the risk-on mentality across risk assets, but we remain concerned that stubborn inflation may not allow the Fed to cut as much as expected. Historically, it has marked the beginning of the end for the credit cycle when growth is strong, central banks are significantly tightening liquidity (or have), and credit risk premiums are smaller, all conditions that are currently present. Our proprietary investment grade and high yield risk premium models currently suggest that the market has little to no expectations for impending credit stress, mainly due to tight spread levels and less a function of forward looking loss estimates.

Given this analysis, we are running lower than average risk positions in our global corporate portfolios given the reduced value proposition. Our primary alpha generating focus centers on issuer relative value swaps, targeted industry plays, cross-currency opportunities, and new issue concession harvesting. Industry rotation to more non-cyclical spaces such as Food, Beverage, and Pharma from more cyclical areas including Basic Industries and Transportation has been a theme over the past year or so. Finally, we remain positive on Banking given the embedded safeguards of capital requirements mandated by regulators but have moved up in capital structures from subordinated to senior issues.

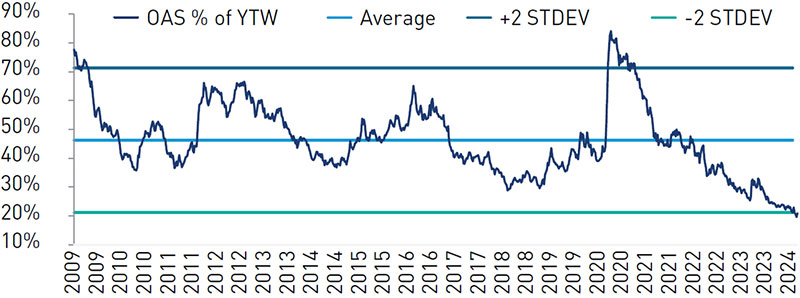

In our view, the overwhelming demand for credit given the relatively attractive yields on offer has provided a strong tailwind. However, the chart below indicates the fact that the bulk of yield has derived not from the embedded risk premium in corporate bonds, but from the underlying government bonds. The question to ask is whether this technical support has pushed corporate bond spreads tighter than fundamentals warrant given the myriad of risks presently. Credit quality has held up reasonably well to this point given the underlying strength of the US economy, but caution is warranted, in our view.

Bloomberg BAA Corp, USD OAS (BPS)* as % of YTW

* OAS is option adjusted spread.

Source: Bloomberg, February 29, 2024

Used with permission from Bloomberg. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Past performance is no guarantee of future results.

There is no guarantee that the investment objective will be realized or that the strategy will generate positive or excess return.

Markets are extremely fluid and change frequently.

Past market experience is no guarantee of future results.

Diversification does not ensure a profit or guarantee against a loss.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice. Market conditions are extremely fluid and change frequently.

Additional notes

This material has been provided for information purposes only to investment service providers or other Professional Clients, Qualified or Institutional Investors and, when required by local regulation, only at their written request. This material must not be used with Retail Investors.

To obtain a summary of investor rights in the official language of your jurisdiction, please consult the legal documentation section of the website (im.natixis.com/intl/intl-fund-documents)

DR-63615

All back to bonds?

All back to bonds?

Sustainable Investing: Still playing the long game?

Sustainable Investing: Still playing the long game?

2024 Private Assets Report

2024 Private Assets Report

Investment Outlook: Loomis Sayles

Investment Outlook: Loomis Sayles